Greenspan: Repel the Calls to Contain Competitive Markets

Hussman Weekly Market Comment (Last Week)

Roubini Interview with Barrons

Fergusson: How a Local Squall Might Become a Global Tempest

The Four Part Series: The Big Freeze

El-Erian: Crisis and Coherence

US inflation is not going away anytime soon

Rogers: Fannie Plan a Disaster

Fed Holds its Breath on Inflation

The preceding chart of spot EUR/USD for the last 10 days is not much to write home about, but when you consider this recent item of news, I'm fairly optimistic. I entered the trade mid-day on May 7th at basically the same level we are currently trading. Initial resistance is at 1.53 with support at 1.5530. I suspect that if negative news in the U.S. propels EUR/USD back to the 1.60 level, it's very possible that there will be a coordinated central bank intervention. I see this is a reasonable floor on my downside. If we can break through the initial resistance of 1.53, sub 1.50 would not be out of the question. I'd likely take profits in the 1.48-49 area. The chart looks a little better when you zoom out:

I'm not expecting EUR/USD to be trading sub 1.40 anytime soon. I'm still a dollar bear. But I feel like the following are coming together to make a short EUR/USD trade compelling:

The longer we are able to stay below this 1.5530 level the more likely I feel we'll be able to take out the 1.53 lows. I am going to Greece tomorrow for 2 weeks so I won't be able to actively watch (this might be a good thing), but even so I have not put any stops in. This move has largely been motivated to put a lid on oil's recent surge. I'm not putting any money into play but I think it's possible oil could be the next trade that has solid investor support to capitulate and pull back. We saw that with the front end of the curve across the world recently. If oil actually does have a pullback this would be extremely USD bullish.

On a different note, I put in some limit sell-short orders on SPY, pyramiding up from 141 to 144. I'm not ready to say that this little counter-trend rally is over but I'm not intent on selling at current levels, especially after the trading of the past couple days. So that's the reason for the pyramiding up. Frankly, I'm hoping they all get triggered because I think it would mean more upside in the long run.

Some other ideas have continued to nag at me. I think the large-cap small cap trade is still looking good, and a consumer cyclical / S&P spread trade seems about right too. If the bulls can take us up past 1420 again I'd be much more likely to put those ideas to work. I'm also assuming any increase to those levels would be driven by discretionary and financials. If that were the case buying a small amount of puts on some of the more unsavory financial names wouldn't be a bad idea.

In the meantime, my risk level is relatively small. I still have my long term rate trades, and those are showing nice gains. This past week was quite a good one for the ol' P/L. But I can't concentrate too much on that in the short term. What matters is that I hold conviction in my ideas and I don't overtrade.

Vallejo, CA officials vote to file for bankruptcy

The short view: Crunchy Credit

Yield of 4% Beckons in Treasurys

Seeing Inflation Only in the Prices that Go Up

Win Some, Lose Some - How to Come Out On Top

Cyclicals are Still Overpriced

Soros Says Impact of Crisis on Economy Just Starting

Home Improvement Investment has a Significant Downside Potential (Short HD?)

U.S. Consumer Debt Surges in March

Silver: Still dependent on gold for upside

Peruvian Miners set to strike May 12th. Silver should see benefits

World Silver Survey authors say silver outlook is still positive

Current Thoughts:

*Home Improvement Stocks look like good short candidates

* I really like how I'm positioned right now (short EUR/USD, long my FF future spread trade, and long Dec ED futures). I'm feeling a little less bullish on my SLV holding. Gold is tracking pretty closely to USD movements, especially EUR/USD.

Caroline Baum: Wall Street CEO Chorus is Singing Out of Tune

What are corporate bonds worth in a recession? (Spreads Have Further to Tighten)

Slow German Growth Sounds Poverty Alert

Weyerhaeuser's Loss - WY is on my value watch list

Tentacles of Recession and the Great Unwind

John Authers: Uncertainty in markets

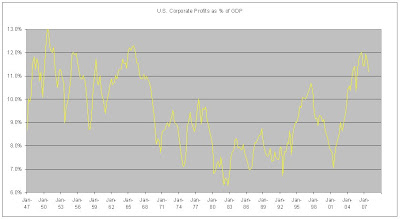

The chart above is Corporate Profits as a % of GDP. When I mentioned above that corporate profits have topped out this is some of the data that helped me come that decision. And this is one of my strongest arguments for why earnings expectations are too high for the latter half of this year. In the Barron's Big Money institutional poll all the bulls were pointing to low P/E's. 55% thought stocks were undervalued. I come to the conclusion that with normalized corporate profits stocks are overvalued. The chart says it all. We are at the highest level of corporate profits since the 60's. And with consumer spending (and leverage in recent years) being the primary driver of corporate profits, do I think these elevated levels are likely to stabilize and continue? I find this unlikely. The chart above (via John Mauldin) makes me think that we have probably topped out in consumer spending as well. The negative wealth effect, stagnant wages, and higher commodity costs all add to the consumer's pain. The economy was essentially fueled in 2002 to 2007 by leverage and HEW's as consumer's thought housing prices would increase forever. HEW's have dried up and as BofA noted in the earning's calls, we have seen rising credit card delinquencies (especially in housing bubble areas). As Bud Fox said, "I'm tapped out Marv. American Express has got a hitman looking for me."

I find this unlikely. The chart above (via John Mauldin) makes me think that we have probably topped out in consumer spending as well. The negative wealth effect, stagnant wages, and higher commodity costs all add to the consumer's pain. The economy was essentially fueled in 2002 to 2007 by leverage and HEW's as consumer's thought housing prices would increase forever. HEW's have dried up and as BofA noted in the earning's calls, we have seen rising credit card delinquencies (especially in housing bubble areas). As Bud Fox said, "I'm tapped out Marv. American Express has got a hitman looking for me."

I have to be wary here about confusing my economic outlook with my market outlook. While ultimately the economics are the underlying factor, the great bull party may continue for a little while longer. I am prepared and will position the portfolio accordingly. Opportunities abound in this market and I am confident I'll be able to take advantage of them.

EUR/USD has fallen 3 big figures in the past 2 days (Just in time for my long EUR/USD post)

A Nice Quick Update on Housing - Peak to trough I think housing prices will fall 25% - 30%

More on March Existing Home Inventory

Japanese Banks Step up their Lending

Banks to Pay Steep Cost in BOE Plan

Economic Recovery Already Underway - I think I may just have to come back to this post in a year or so for humor

Quite a disparity between domestic and foreign YoY profit growth. Makes a very compelling case for my short Russell trade and less of a case for my short DOW trade. Macro Man recommends a large cap/small cap spread trade. Now that might work for me If I had a big capitalization but I have a pretty small account. I'm more likely to just cut my short DOW trade and keep my Russell 2,000 short on.

Quite a disparity between domestic and foreign YoY profit growth. Makes a very compelling case for my short Russell trade and less of a case for my short DOW trade. Macro Man recommends a large cap/small cap spread trade. Now that might work for me If I had a big capitalization but I have a pretty small account. I'm more likely to just cut my short DOW trade and keep my Russell 2,000 short on.

I'm feeling pretty comfortable right now with my short equities position. Falling domestic profits, elevated valuations, and what will likely be slower consumer spending all lend support to my trade.

If we see some big upward surprises tomorrow before the market opens for Caterpillar, Citigroup, and Honeywell we could have a pretty big up day for U.S. equities.

On the international front, Iceland's credit rating was cut again by S&P and Israel's rating was raised by Moody's. Now I don't necessarily care too much about what the soon-to-be-defunct-in-current-form rating agencies are doing, but I was planning on taking this weekend to read up on Israel and their market. My initial thoughts were that Israeli equities were pretty darn cheap. Along with Israel, South Korea and Turkey are on my agenda. South Korea is dirt cheap, but they are also closely tied to the fortunes of Samsung. I plan on checking out the macro picture in addition to looking at equities, currencies, etc. etc. for those three countries. I'm hoping to make this a weekend ritual actually.In currencies, Luxembourg Finance Minister Jean-Claude Juncker helped lift USD by saying financial markets misunderstood the recent G-7 statement about currency volatility. I've believed for some time that the endgame for the slide of USD is cooperative action by the world's central banks. This would certainly make that statement by Juncker pretty important. But we're not quite there yet. Macro Man has a good post on the wording of past statements preceding currency interventions. I mentioned this idea to a friend who works in currencies and he brought up an essential point that even if their was collective action to boost USD, China is sitting on over $1 Trillion and will buy EUR/USD out to yazoo. This makes collective action extremely difficult.

So that's the portfolio right now. Won't be doing any other moves in the near future. I am moving the portfolio to MB Trading over the course of the next two weeks. As I've mentioned before, I'm approved for margin trading, futures, options, and international markets over there. This is the initial setup for the portfolio during the ACAT transfer process. As with any shorts, I'll be keeping a close eye to make sure things don't get out of hand. Since these are all long/medium term holdings, my plan is to do a thorough review of a position if I it's at a 10% unrealized loss.

So that's the portfolio right now. Won't be doing any other moves in the near future. I am moving the portfolio to MB Trading over the course of the next two weeks. As I've mentioned before, I'm approved for margin trading, futures, options, and international markets over there. This is the initial setup for the portfolio during the ACAT transfer process. As with any shorts, I'll be keeping a close eye to make sure things don't get out of hand. Since these are all long/medium term holdings, my plan is to do a thorough review of a position if I it's at a 10% unrealized loss.

Earnings estimates clearly lag actual earnings by about a year. And this becomes pivotal in tops and bottoms. As you can see from the chart it's clear that sentiment hasn't really caught up with the decline in earnings. Read the entire piece via John Mauldin and you can see some reasons for this. It's pretty interesting stuff.

Earnings estimates clearly lag actual earnings by about a year. And this becomes pivotal in tops and bottoms. As you can see from the chart it's clear that sentiment hasn't really caught up with the decline in earnings. Read the entire piece via John Mauldin and you can see some reasons for this. It's pretty interesting stuff.

Does the U.S., especially the NASDAQ, deserve a higher P/E than China? As far as I am aware China's economy is growing at double digits while our economy has negligible growth. Remember my previous post about market returns YTD. This entire situation doesn't make a lot of sense to me. Yes, a lower dollar is helping exports and U.S. companies are not nearly as tied to the domestic economy as they used to be, but still....

Across the board the street is still expecting higher equity markets by the end of the year. Merrill's Thain recently said that the worst of the credit crisis is behind us, but I think we're probably only about half way through. Housing prices still have not stabilized. Today's pending home sales numbers fell more than expected. This is just one of countless examples of a housing market that is in the early to mid stages of a depression.

{kind=link}