Fed set for further cut in rates

View of the Day - Ian Scott, Lehman Brothers

Safety dash into bonds brought to abrupt end

Wrigley Mars Deal in Depth - 32 x forward earnings and 20 x ebitda seems darn pricey to me

Soaring Rice Prices Send Asian Nations Scrambling

Is the Work of Fed Bankers Really Done?

DB Chief Energy Economist: Oil to $250, then demand collapse

Barron's Big Money institutional survey - Quite telling. I find myself in disagreement with many of these big time money managers. As one commentator put it, "many of these guys appear to be trading the rally before we've experienced the recession." I agree.

Bill Gross' May Investment Outlook - "Home prices and their real economic fallout are the financial markets – and PIMCO’s – vulnerable flank." I'm glad I'm on similar terms. I have taken a side on this issue and feel that falling home prices will lead to economic fallout in consumer spending and corporate profits. Indeed, these two indicators have already topped out. This is basically the core of my domestic outlook for equities. And to continue, I think that this is our endgame:

"To be brief and blunt, the reason that home prices are so critical, he would claim, is that they are at the forefront of potential asset deflation. Because the U.S. and selected other economies are now substantially asset-based and dependent on stable and upward tilting prices, a deflation of an economy’s primary financial asset can be ruinous. Its deflationary thrust must be countered, wrote Minsky, or else the battle might be lost. If so, the real economy as Mohamed El-Erian suggests, might become so shell-shocked that financial markets once again turn down instead of up."

I don't necessarily think that we will have a long-term deflationary problem like Japan. But I think it's likely declining home prices will lead to slower consumer spending, the great "muddle-through" economy combined with the great unwind in leverage, and lower financial asset prices as a result. My short equity bias remains as long as I view earnings expectations to be overly optimistic. Currently I view Q3-Q4 as wildly optimistic. I'm less inclined to believe Q2 will be greatly below expectations because of the effects of the stimulus checks. Even that argument contains less merit as oil continues to hover around $120 and gas remains around $3.60/gallon.

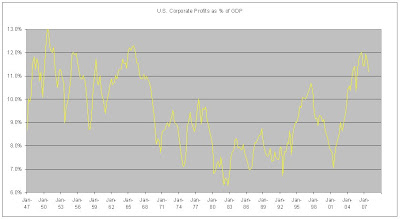

The chart above is Corporate Profits as a % of GDP. When I mentioned above that corporate profits have topped out this is some of the data that helped me come that decision. And this is one of my strongest arguments for why earnings expectations are too high for the latter half of this year. In the Barron's Big Money institutional poll all the bulls were pointing to low P/E's. 55% thought stocks were undervalued. I come to the conclusion that with normalized corporate profits stocks are overvalued. The chart says it all. We are at the highest level of corporate profits since the 60's. And with consumer spending (and leverage in recent years) being the primary driver of corporate profits, do I think these elevated levels are likely to stabilize and continue? I find this unlikely. The chart above (via John Mauldin) makes me think that we have probably topped out in consumer spending as well. The negative wealth effect, stagnant wages, and higher commodity costs all add to the consumer's pain. The economy was essentially fueled in 2002 to 2007 by leverage and HEW's as consumer's thought housing prices would increase forever. HEW's have dried up and as BofA noted in the earning's calls, we have seen rising credit card delinquencies (especially in housing bubble areas). As Bud Fox said, "I'm tapped out Marv. American Express has got a hitman looking for me."

I find this unlikely. The chart above (via John Mauldin) makes me think that we have probably topped out in consumer spending as well. The negative wealth effect, stagnant wages, and higher commodity costs all add to the consumer's pain. The economy was essentially fueled in 2002 to 2007 by leverage and HEW's as consumer's thought housing prices would increase forever. HEW's have dried up and as BofA noted in the earning's calls, we have seen rising credit card delinquencies (especially in housing bubble areas). As Bud Fox said, "I'm tapped out Marv. American Express has got a hitman looking for me."

I have to be wary here about confusing my economic outlook with my market outlook. While ultimately the economics are the underlying factor, the great bull party may continue for a little while longer. I am prepared and will position the portfolio accordingly. Opportunities abound in this market and I am confident I'll be able to take advantage of them.